As an ERISA attorney, people sometimes ask for a sample administrative appeal letter. So hopefully you’ll find this helpful! This sample appeal letter structure can be used whether you’re appealing the denial of disability insurance benefits, life insurance benefits or accidental death insurance benefits that fall under ERISA law.

A little context is helpful to understand the sample appeal letter below. Maybe it will even sound familiar to your situation, as we come across variations of the same scenario regularly in wrongfully denied life insurance claims.

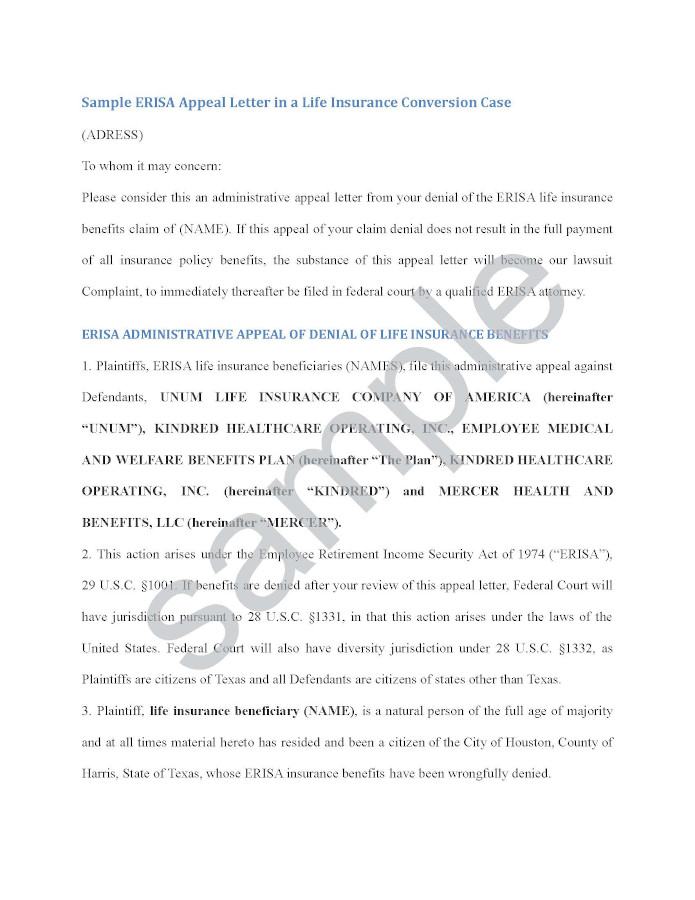

This particular appeal letter is from a case where we represented two really nice ladies on a life insurance claim denial after their deceased mother’s employer and UNUM life insurance company failed to offer her “conversion” from the employer’s group ERISA life insurance policy to an individual policy. Our clients’ mother had gone out of work on long-term disability with a terminal illness, and died from it about 10 months later. When she stopped working, under her employer’s ERISA insurance “Plan,” her employer was required to offer her “conversion” of her life insurance policy.

For a free legal consultation, call (225) 201-8311

Conversion is when someone who is covered by an insurance policy issued as part of an ERISA employment benefits plan stops working for the company, whether because of disability or other reasons. They can choose to continue coverage under the same insurance policy by converting the group insurance policy to an individual policy by paying the premiums directly to the insurance company instead of paying through deductions from paychecks.

So the policy “converts” from a group policy to an individual policy for the insured, but provides the same coverage, because the insured is no longer part of the “group” once employment ends. If a person leaves employment because of retirement, they can usually continue individual coverage in similar fashion to converting, but the insurance policy usually refers to this as “porting” their coverage under retirement circumstances.

Well in this case, the employer messed up. The HR department told our clients’ mother that all she needed to do to keep her life insurance with UNUM after going out on disability was to pay premiums to the employer, and the employer would pay UNUM to keep the life insurance coverage in effect.

ERISA Lawyer, J. Price McNamara

Click to contact our insurance claim lawyers today

So my clients’ mother paid monthly premiums to the employer as instructed. Problem is, the employer failed to pay UNUM. Since our clients and their mother knew that she was dying, they made sure they strictly followed the advice of HR to keep the life insurance policy in place. But the advice was wrong.

When our clients’ mother died, they presented their claim to UNUM, but were shocked to learn that UNUM claimed that no life insurance policy was in effect because they did not receive any premium payments, nor the required conversion paperwork from HR. So UNUM denied the claim.

Complete a Free Case Evaluation form now

A couple of important points about the sample appeal letter below: You’ll see that this sample appeal letter is long, and sets forth every detail of the lawsuit that will be filed in federal court if the insurance company denies the administrative appeal. Note that we include reference to the insurance policy language at issue in the claim denial, as well as detailed facts to show the insurance company why your claim has undeniable merit, with specific page references to our evidence and administrative record and claim file. The appeal letter is even structured to read exactly like the lawsuit will read if they persist in their denial.

![]() This approach brings several advantages. First, it lets the insurance company who denied the claim know that we are serious and know what we are doing under ERISA law. Second, it tells the insurance company exactly why it will lose in federal court under ERISA law if they do not agree to pay benefits. Third, it lets us file the lawsuit in federal court immediately if they do deny the claim on appeal. It’s ready to go. This moves us faster along the path toward final resolution by court judgment.

This approach brings several advantages. First, it lets the insurance company who denied the claim know that we are serious and know what we are doing under ERISA law. Second, it tells the insurance company exactly why it will lose in federal court under ERISA law if they do not agree to pay benefits. Third, it lets us file the lawsuit in federal court immediately if they do deny the claim on appeal. It’s ready to go. This moves us faster along the path toward final resolution by court judgment.

This sample appeal (and lawsuit, if need be) names the ERISA “Plan,” the ERISA “Plan Administrator” and the insurance company who insures the ERISA Plan as well as responsible parties.

***The appeal letter should be addressed exactly as instructed in the benefits denial letter, and sent by certified mail, along with any other electronic means of delivery provided by the insurance company who denied the claim.

***REMEMBER, your appeal letter should include copies of ALL EVIDENCE you can provide to support your claim, and detailed reference to the page numbers of that evidence you provide.

***Why? Because if the insurance company denies your administrative appeal, you can file an ERISA lawsuit in federal court, BUT the court cannot consider any evidence that you did not present and make part of the “administrative record” to be considered by the insurance company before filing your lawsuit. In this case, we provided affidavits (sworn statements) of our clients, as well as copies of all referenced documents, referring to them by specific page number, to support every factual allegation.

We hope you find this sample appeal letter helpful!

Call us or shoot us an email if we can answer any questions about your administrative appeal letter or claim. We’ll be happy to talk. ERISA LAW IS ALL WE DO!

Call or text (225) 201-8311 or complete a Free Case Evaluation form