How Physicians Can File a Successful Disability Insurance Claim or Appeal a Claim Denial

To Physicians Stuck in a disability insurance claim battle…

Take a note of hope from a former insurance company attorney (and proud husband and more recently father of two physicians), who now helps doctors and other healthcare providers win their long-term disability benefits claims, appeals and lawsuits nationwide:

Receiving a denial letter does not mean it’s over – not even close – you can overturn an unfair claim denial!

Disability insurance companies follow the same playbook to deny valid physician claims every day, knowingly interpreting their disability policies to find the physician-claimant “not disabled under the terms of the policy” even when the law clearly provides that you are.

Whether it’s a short- or long-term disability claim, YOU know your medical condition renders you disabled from adequately performing the full spectrum of the essential duties of your profession. And your own treating physicians – highly-trained specialists in the field of your disabling medical condition agree that you’re disabled.

So it’s a terrible feeling – You’re shocked by the disability insurance company’s denial letter while you’re handling the financial and emotional stress that comes with your disabling medical issue.

The denial letter likely over-generalizes your occupation, and glosses over the true rigorous physical and cognitive demands of your occupation, as actually performed. The denial probably relies on the opinions of the insurance company’s own doctors, who disagree with you and your treating physicians about your true physical and cognitive restrictions and limitations. And those doctors are often not even specialists in your own field, or in the specialty field of your medical condition.

Most of the physicians’ disability claims we’ve reviewed and fought have presented variations of that same script.

Whatever excuse they’re giving you, you’re thrown into the legal world of insurance policy definitions, administrative appeals, and likely, federal “ERISA” law.

You want to get the next steps right without guessing, and you’re exhausted by their claim process, as they want you to be.

But persevere – the insurance companies are often WRONG or BREAKING THE LAW, and if so you CAN overturn a denial.

The Win My Benefits Process, what we use and consider to be “best practices” for securing benefits or appealing a denial, is described below. You can use it as a guide, or contact us if you’d like help.

[video_block popup="false" video="For a free legal consultation, call (225) 201-8311

Why Physicians are Special Targets for Unfair Claim Denials – The Big Picture

As a doctor or other medical professional who has filed a disability insurance claim, you’ve likely learned that the insurance company will distort reality to deny your legitimate claim.

Medical professionals and providers, from physicians, nurse practitioners, physician’s assistants, certified nurse anesthetists, dentists and nurses are especially targeted by the insurance companies for denial, because their earnings are high relative to the typical disability insurance claimant.

In fact, the same goes for attorneys, executives, and many others whose incomes are above the mean. The higher the claimant’s income, the higher the monthly disability benefit, and the more costly it is to the insurer’s bottom line. And with most policies entitling you to benefits to age 65 or normal retirement age of 67, just one claim can easily cost hundreds of thousands to millions of dollars over the life of the claim.

Multiply that by the huge number of claims the insurer denies each year across the country, and… you get the picture. Their entire business model involves maximizing premium revenue while minimizing claim payment costs. Your claim is just another cost. Denying your valid claim affects their bottom line the same as denying an invalid one.

To combat the high cost of paying benefits, many insurance companies write long-term disability policies for healthcare providers with provisions that serve as a high hurdle for getting their claims approved. And if your claim is governed by federal ERISA law (short for the Employee Retirement Income Security Act of 1974), as most are, another layer of difficulty is added to getting your claim approved as discussed below.

Disability Insurers Intentionally Design Their Claim Process to Lead Physicians Down a Path to Claim Denial

The truth is, insurance company wants you confused and exhausted by their claim process.

Their denial letter tells you that under “ERISA law” you can “appeal.” But they obviously don’t want to pay your benefits, so they give you no guidance on HOW to appeal with any chance of winning. And at issue is a substantial sum of money.

So you wonder: How long should an appeal be? What should I say? What traps should I avoid? What additional records, expert reports, witness statements or other evidence will help me win? Do I even have a chance of recovering my benefits?

The good news is, you can still win the insurance benefits you paid for to protect your livelihood and your family despite receiving a denial letter. The LAW, not the insurance company, has the last word.

Every unique claim has a unique best path for best chances to recover benefits and financial security for your family.

But there are also paths to avoid – the paths where your insurance company intentionally tries to lead you, likely resulting in permanent loss of those benefits.

Our goal here is to eliminate the anxiety and exhaustion that comes from uncertainty, and to guide you to your best path to the benefits you paid for without making common mistakes.

As a Former Insurance Company Attorney, I’ll Tell You Their Playbook – How they Hope You React to Their Denial Letter, and What You Should Do Instead. (Don’t Skip This…)

The insurance company hopes you’ll react to its claim denial, now that they’ve exhausted you, in one of two ways – call them the two paths to certain claim denial:

1. You give up or delay, letting your appeal deadline expire; or

2. You file an “appeal” that simply argues why the claim denial was wrong, without submitting stronger new EVIDENCE (most claimants, and attorneys unfamiliar with federal ERISA law, make this mistake).

The insurance company knows that by choosing either of those two paths, you will lose your last and best chance of getting benefits.

The first path for certain claim denial: If you let your appeal deadline (usually 180 days from your receipt of the denial letter) expire, your claim is over. You have no further recourse, and cannot bring a lawsuit in court. The appeal is mandatory before filing a lawsuit, but if you miss the appeal deadline, you can no longer appeal or file a lawsuit. A huge number of claims are lost by simply waiting too long to appeal.

The second path for certain claim denial: If you “appeal” by submitting argument alone, without new, stronger EVIDENCE, the insurance company knows that ERISA law prohibits the court from considering any evidence that you didn’t submit with your appeal before filing suit. Thus, appealing in this manner is a trap. By doing so, you lock yourself out of building the strongest claim you can for good. Most claimants and attorneys unfamiliar with ERISA law don’t realize this until it’s too late. Therefore, most put little effort into the appeal process, mistakenly thinking they can get serious about building a strong court case later if the appeal is denied. You can do that in a “normal” case not falling under ERISA law, but under ERISA law, everything is different.

This ill-advised “appeal” approach, with argument alone and little or no new evidence, is often the product of waiting too long. A well-built appeal requires thought, strategy, and time as you’ll see below. Letting the deadline sneak up on you, and quickly throwing something together to meet it, is the worst possible way to approach preserving your right to years of critical financial benefits.

The tragedy is, neither your insurance policy, nor your denial letter will tell you any of this. But your insurance company knows all about it, and is happy to sit back watching as you fall into these traps.

If fact, they’ll even lead disabled physician claimants down this second path for certain claim denial. I can’t tell you how many times clients have told me, “After the initial claim denial, the insurance adjuster called, was really friendly, and told me not to worry. She said that initial denials are common, that I had a strong case, and I didn’t really need an attorney – all I had to do was write a quick appeal and send it in.”

Insurance adjusters who say that know exactly what they’re doing. They are not your friend in this process.

But there’s a third path. It’s what the insurance company DOESN’T want you to do, and it’s exactly what you SHOULD do for best chances of claim approval.

This third path is to BUILD your claim and appeal strategically with NEW EVIDENCE (not just ARGUMENT), using a tested and successful PROCESS that PROVES your claim the way they know has the best chance to stand up in court if they deny your appeal.

That’s what wins benefit claims – as well as appeals and lawsuits, and the years of future financial security you paid to protect. But avoiding pitfalls and getting it right is critical.

Below is a brief but important overview of Physicians’ disability insurance coverages and important policy provisions, followed by our step-by-step Win My Benefits process to build a strong claim or appeal a denial of benefits.

We’ll cover the following:

Click to contact our insurance claim lawyers today

Physicians’ Disability Insurance Policies and Core Provisions: An Overview

1. Short-term vs. long-term disability insurance

2. The key policy provisions that drive a physician’s long-term disability claim: “Disabled,” “Disability,” and “Own Occupation” (or “Your Occupation”)

A. True Own-Occupation Definition of Disabled or Disability

B. Transitional Own-Occupation Definition of Disabled or Disability

C. Modified Own-Occupation Definition of Disabled or Disability

D. Any Occupation Definition of Disabled or Disability

E. Illustrated Comparison of How the Different Common Definitions of Disability Work

The Fight: The Most Commonly Disputed Issues in a Physician’s Disability Insurance Claim Denial with Examples

1. The common issues in the physician’s disability claim dispute

2. Examples of typical physician’s disability claim dispute fact scenarios

3. Our emergency room physician client’s recent dispute with Prudential is a classic example

Federal ERISA Law, and its Impact on Physician Group Disability Policy Claims: a Critical Distinction with Big Consequences

1. Why different laws apply to group and individual policies and why it matters

2. What the insurance company hopes you don’t know about federal ERISA law until it’s too late

3. What is so different about an ERISA disability insurance case?

THE CLAIM PROCESS

THE ADMINISTRATIVE APPEAL

THE FEDERAL COURT LAWSUIT…

Complete a Free Case Evaluation form now

A Step-by-Step Process for a Physician to Win an ERISA Disability Claim – Shredding the Insurance Company Playbook and Beating Them at Their Own Game

1. Calendar your appeal deadline

2. Analyze the insurance company’s denial letters

3. Analyze the insurance company’s claim file or administrative record

4. Analyze the long-term disability insurance policy, plan and summary plan description

5. List the foundational information supportive of your claim

6. Gather and analyze medical records to see how well they support the claim for disability and supplement where needed

7. Decide what additional evidence may be helpful

8. Conduct legal research

9. Construct the best argument

10. Final review

11. Submit the best argument and await a decision

Physicians’ Disability Insurance Policies and Core Provisions: An Overview

1. Short-term vs. long-term disability insurance

You may be filing a new claim, or have received a denial for either short- or long-term disability insurance coverage. Both short- and long-term disability insurance cover a percentage of your income if an illness or injury disables you from working.

As the names suggest, short-term disability and long-term disability insurance are distinguished by how long they pay.

Short-term disability insurance coverage usually begins a week after the disability begins and continues for just a few months, usually between 90 and 180 days after the disability starts. In most policies, it replaces 50% – 80% of your income for the period you have coverage.

Long-term disability insurance coverage starts after short-term coverage ends, if a more serious illness or injury prevents you from working as a physician for an extended period of time. It lasts until either you can return to some degree of work (depending on your policy’s definition of “disability” or “disabled,” a key provision affecting your claim, especially as a doctor, as discussed fully below), or until the end of the benefit period – typically either age 65 or “normal retirement age” if you remain disabled for that long. Long-term disability coverage typically pays 60-66% of your income at the time you became disabled.

Long-term disability insurance is critically important to have because it covers catastrophic disabilities that can keep you out of work as a doctor for years, or permanently.

2. The key policy provisions that drive a physician’s long-term disability claim: “Disabled,” “Disability,” and “Own Occupation” (or “Your Occupation”)

The success of a doctor’s long-term disability insurance claim is most heavily impacted by the definitions of “Disability” or “Disabled”, and “Own Occupation” or “Your Occupation” found in the policy. These definition provisions vary from policy to policy. In order for you, as a physician to qualify for disability insurance benefits, you must meet the definition of “Disability” or “Disabled” outlined in your policy.

If you’ve received a claim denial, your insurer should have quoted these defining provisions in your denial letter. Knowing exactly what YOUR provisions mean is key to knowing exactly what evidence and proof (not just argument) you, as a doctor, must BUILD into your claim or appeal record, medically, factually and legally in order to succeed in recovering long-term disability benefits.

The four most common different types of definitions of disability in physicians’ long-term disability policies are:

- True own-occupation

- Transitional own-occupation

- Modified own-occupation

- Any occupation

While different policies provide slightly different variations of each type of definition, in large part they work the same way.

Here’s how each type of definition applies:

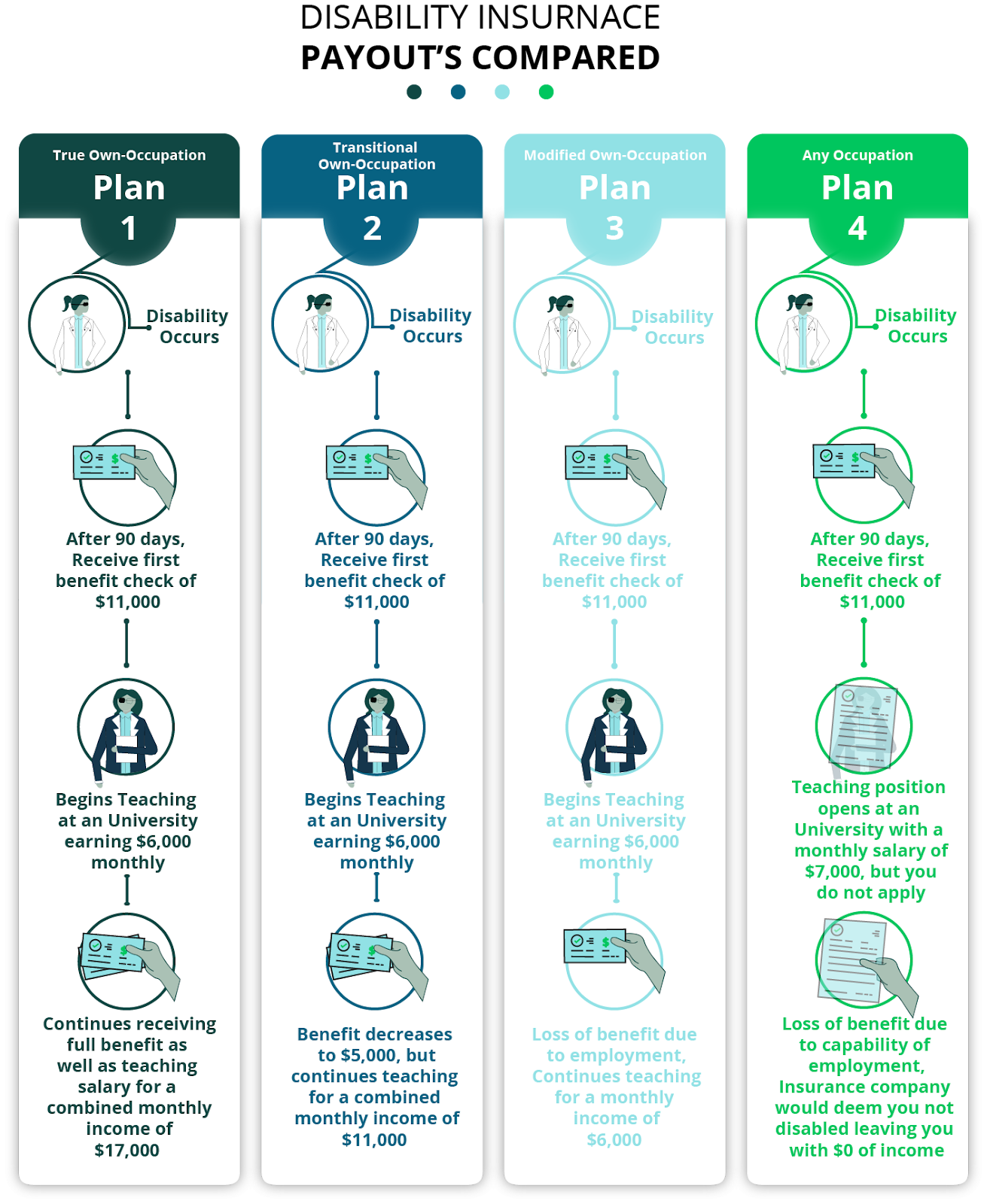

A. True Own-Occupation Definition of Disabled or Disability

“True own occupation” coverage provides the strongest disability insurance protection for physicians. Since true own occupation long-term disability policies for physicians offer the broadest coverage and protection, they’re also the most expensive to purchase. A true own occupation definition of disability will clearly define you as totally disabled if you can’t perform the duties of your “own occupation” on a full-time basis, with “own occupation” meaning your specialty or sub-specialty.

The language of each contract can vary, but a true own occupation definition of “total disability” or “totally disabled” will read something like this:

“You are not able to perform the material and substantial duties of your Own Occupation. You will be Totally Disabled even if you are Gainfully Employed in another occupation so long as, solely due to Injury or Sickness, You are not able to work in your Own Occupation.”

True own-occupation coverage pays you your full benefit if you can’t perform the specific duties or specialty, even if you’re practicing medicine and earning a salary, even the same salary, in some other capacity. You’ll still be considered disabled and get your full benefit payout.

Take, for example, a cardiovascular surgeon with a disability preventing him or her from performing surgery, but who is still capable of working as a general cardiologist or cardiology professor. Under a true own occupation long-term disability policy, that cardiovascular surgeon is entitled to full policy benefits even if working as a general cardiologist or cardiology professor, and even if earning the same amount as he or she did as a cardiovascular surgeon.

There are a few other definitions of disability that can be confused or even mistakenly sold as true own-occupation disability insurance to doctors. However, these policies won’t continue to pay your full benefit if you can perform other jobs, even if they are lower-paying jobs.

B. Transitional Own-Occupation Definition of Disabled or Disability

With this definition, your policy will pay benefits similar to a true own-occupation policy with one important difference: If you can’t work in your specialty, but you start earning an income doing something else, your total net income, including benefits, cannot exceed the total income of your former job.

A transitional own-occupation policy will include a provision something like this:

“You will continue to receive disability benefits if you become totally disabled from Your Occupation, but are working in another occupation. Benefits will be paid up to 100% of your prior earnings, but will not exceed the total monthly benefit.”

With transitional own-occupation coverage, the policy will generally cover your income up to the point of your income before the disability. As an example, prior to your disability, say you were making $12,000 a month. After your disability, you began working as a professor earning $6,000 a month. If you weren’t working at all due to your disability, and your policy benefit was 60% of prior earnings, it would pay $7,200 a month. But with your professor salary, a transitional own-occupation policy would then pay you only a $6,000 monthly benefit, because when added to your $6,000 monthly income from teaching, the sum would total your prior $12,000 monthly income.

Essentially, with a Transitional Own Occupation policy, you can take advantage of a new job opportunity while still getting your benefit. The difference is that the company will only pay the gap between your old monthly income and your new monthly income.

C. Modified Own-Occupation Definition of Disabled or Disability

In a modified own-occupation policy, the definition of disabled will read something like this:

“The Insured is Totally Disabled when both unable to perform the principal duties of his or her Regular Occupation and not Gainfully Employed in Any Occupation.”

Under this type of coverage and definition, benefits do not continue if the doctor becomes “Gainfully Employed” in another occupation – “Any Occupation”. Thus the options for a totally disabled physician with modified own-occupation coverage would be to either live off their benefit check, return to their “Regular Occupation,” or become “Gainfully Employed” in a different occupation without receiving their disability benefit. If the disabled physician becomes “Gainfully Employed” in a different occupation, such as in the cardiovascular surgeon-turned professor example above, benefits would cease under a modified own-occupation Policy.

One important caveat: “Gainfully Employed” is sometimes defined in disability policies to include an income threshold component, whereby the insurer can’t deny benefits on the basis that the claimant is performing the duties of any job, at any wage. Rather, to warrant termination of benefits, the physician must be earning above a certain amount, typically 80% of their pre-disability income.

D. Any Occupation Definition of Disabled or Disability

Under an any-occupation policy, you’re considered disabled only if you can’t work in any occupation for which you could be considered reasonably suited based on education, training, or experience.

The definition of disabled an any occupation policy will look something like this:

“You are unable due to illness or injury to perform the material and substantial duties of any occupation for which you are reasonably fitted by education, training, and experience.”

Thus, if you’re able to work in another industry and there are open positions that you’re capable of performing within your medical restrictions and limitations, the insurance company will argue that you’re no longer be totally disabled under the policy. Whether or not you choose to take the job doesn’t matter.

As with modified own-occupation policies, some any-occupation policies will include an income threshold qualifier, whereby the “any occupation” capability must be for jobs with earnings at or exceeding a certain percentage of the doctor’s pre-disability income.

Look at your own policy to see which definition of “disability” applies.

E. Illustrated Comparison of How the Different Common Definitions of Disability Work

This illustration is for physicians’ long-term disability coverage having a 90-day elimination period.

The Fight: The Most Commonly Disputed Issues in a Physician’s Disability Insurance Claim Denial with Examples

Whether a claim denial involves true, transitional, or modified “Own Occupation” coverage; or “Any Occupation” coverage, the issues at the core of the typical dispute overlap.

1. The common issues in the physician’s disability claim dispute

Sometimes the principal argument in a claim dispute is whether the language of your policy actually provides true own occupation coverage. Key provisions can differ from policy to policy, depending on when they were written and what company wrote them. The precise policy provisions, the policy definitions of any defined terms, usually capitalized in the provisions and defined in a separate section of the policy under the heading “Definitions,” and how courts have interpreted the same or similar provisions in other cases are key.

Don’t think the insurance company will overlook any opportunity to argue these points to avoid paying your claim. Denial disputes may involve some or all of the following issues: the policy definition of “Own Occupation”, and whether it is defined in terms of the physician’s specialty or sub-specialty, or more generally; what exactly are the material and substantial duties of the physician’s “Own Occupation” as properly defined; what are the physician’s true physical or mental restrictions or limitations (including any medication side-effects) in light of the illness or injury at issue; and whether those limitations cause inability to carry out those duties.

If the physician’s regular occupation is a specialty or sub-specialty requiring skills and capabilities the doctor is disabled from performing, but not required in a broader occupational category, the insurer will argue “Own Occupation” to mean the broader category.

Aside from the arguments over whether a physician’s specialty or a more general categorization of physician is appropriate for analysis under the policy provisions, commonly in dispute are the physician-claimant’s restrictions and limitations. The insurance company will usually use the opinions of one or more physicians it contracts to review your medical records to determine your restrictions and limitations, which often contradict the disabled physician-claimant and his or her treating physicians on the issue.

2. Examples of typical physician’s disability claim dispute fact scenarios

As an example, say the physician’s regular occupation may be “urologist,” requiring surgical skills. The insurer will try to categorize his or her occupation generically as a “physician”. If a hand injury would disable the physician claimant from his true occupation as a urologist, but not from the occupation of a family practice physician, an insurer may argue that he or she can still work as a “physician,” and therefore is not disabled under the policy.

As another example, in a recent actual case, the insurance company denied disability benefits to an emergency room cardiologist because he could perform the duties of a cardiologist if not emergency-room based. The court disagreed, holding that emergency cardiac patients required physical capabilities from which the doctor was disabled, that were beyond those required of non-emergency room cardiologists. Therefore, the court found the physician totally disabled from his occupation as an emergency room cardiologist despite his ability to still be a cardiologist.

3. Our emergency room physician client’s recent dispute with Prudential is a classic example

As another example, we recently won an appeal for our client, a Texas emergency room physician, who fought to continue working for as long as he could after major cervical and thoracic spine issues ultimately required multiple surgeries fusing levels C2 – T3. His duties required quick thinking and rigorous physical action, performing orthopedic dislocation reductions, intubations, placing central lines, and lumbar punctures. He also regularly encountered combative intoxicated and drug-altered patients.

His post-laminectomy syndrome pain and medication regimen took their toll. He began to falter physically and mentally until it became impossible for him to safely perform the material and substantial duties of his specialty. Unrepresented, he filed for long-term disability insurance benefits with Prudential after years of premium payments. He explained to Prudential that his pain and increasingly limited mobility endangered his patients. His own treating surgeon opined that he had become “increasingly reliant on a chronic pain regimen, including opioids and other controlled substances to function in even the most basic manner…” and suffered slow, clouded and unreliable thinking as a result. Our physician figured there was no way in the world he’d be denied. Everything he submitted was absolute truth.

But Prudential had its own doctor review his medical records. Without even bothering to meet with our client, Prudential’s physician opined that he could continue his full-time duties as an ER physician. Prudential credited its record reviewer’s opinions over the opinions of our client and his treating providers and denied the claim.

We filed his ERISA-mandated pre-litigation appeal, loading the administrative record with better objective and opinion evidence of his disability, along with more detailed sworn testimony from our client explaining exactly how his restrictions would endanger patients under different specific example scenarios. Prudential reversed its denial, and our client will now be paid monthly through retirement age.

Unfortunately, cases like these are far from unusual. When insurers like Prudential deny physicians’ long-term disability claims, they hope their insured will just “appeal” by arguing disagreement with the denial. They know that ERISA law prohibits the court from considering any evidence not submitted with the appeal before filing suit (most people don’t realize this until it’s too late). Loading the administrative record with the best evidence during the appeal process before filing suit is a critical step to getting claim denials like these reversed, whether on appeal, or in court if the insurance company denies your appeal.

Read on to learn the best process that you, as a doctor, can follow, and common mistakes you need to avoid along the way, to get your claim approved and win the disability benefits you paid for and deserve.

Federal ERISA Law, and its Impact on Physician Group Disability Policy Claims: a Critical Distinction with Big Consequences

1. Why different laws apply to group and individual policies and why it matters

A large majority of long-term disability insurance claims in the U.S., about 80%, are governed by the federal ERISA statute. With a few exceptions, ERISA governs all long-term disability insurance claims involving group insurance policies or plans which form part of a physician’s employee benefits package. Policies that physicians purchase individually on their own are not governed by ERISA. Whether or not ERISA governs a doctor’s claim matters, big time, long before any lawsuit is ever filed.

If the insurance company denies a physician’s initial long-term disability insurance claim governed by ERISA, the administrative appeal, and the federal court lawsuit that follows if the appeal is denied, is a complex minefield for the unfamiliar. Disability insurance companies and their attorneys know and understand how to use ERISA’s complexities to their advantage. But claimants, and often their attorneys, typically don’t until it’s too late.

Unfortunately, many claimants whose claims are governed by ERISA file administrative appeals unrepresented, or represented by attorneys unfamiliar with ERISA law. The result is often the permanent loss of a benefits claim that could, and should have been successful. Understanding the following will help you avoid unnecessary losses.

2. What the insurance company hopes you don’t know about federal ERISA law until it’s too late

One thing the insurance company hopes you don’t realize until it’s too late is the importance of the administrative appeal.

What makes the administrative appeal in an ERISA disability insurance claim so critical? Can’t I always file suit and get serious about building a case later in court if the administrative appeal is denied?

The simple answer is “no”, and that comes as a surprise to many after it’s too late.

What makes the administrative appeal so critical, is that the federal judge in the ERISA lawsuit that follows, cannot consider any evidence that was not made part of the administrative record during the administrative appeal process. So the administrative appeal is your only chance to gather, create and build the best evidence to support your case later in court. The evidence you submit during the administrative appeal process becomes part of that record that the court can later consider. Whatever case you build (or don’t) is carved in stone before you ever file suit.

That the administrative appeal makes or breaks your case cannot be overstated. It is during this process, before a lawsuit can even be filed, that most claimants lose without realizing it.

A brief overview of the life of an ERISA disability insurance claim, and how it’s so different, underscores the importance of the administrative appeal for its success.

3. What is so different about an ERISA disability insurance case?

The process starts when someone files an initial application or claim for disability insurance benefits, usually without attorney assistance, and receives a written denial of their claim by the insurance company.

THE CLAIM PROCESS

Disability insurance policies purchased by physicians on their own, independent of their employment, are not governed by ERISA. For individual disability insurance policies not governed by ERISA, if the insurer denies the claim, the claimant can go directly to state court and file a lawsuit. No “administrative appeal” to the insurance company is required, and there is no requirement that the lawsuit be filed in federal court. Normal state court procedure, including all typical discovery methods are available. The claimant has the right to a jury trial, and all parties can introduce traditional evidence, including live witness testimony. Bad faith penalty remedies are available under state law that are unavailable under federal ERISA law. Typical litigation.

THE ADMINISTRATIVE APPEAL

However, if the claim is governed by ERISA, as most are, a mandatory administrative appeal process is required by ERISA before a claimant can file suit to challenge a denial of benefits. The claimant must file the administrative appeal with the same insurance company that denied the claim. Then that same insurance company, which also must pay benefits if it reverses itself, decides whether or not to reverse itself and pay benefits – crazy but true.

WARNING 1: The deadline for filing an administrative appeal on a denied disability insurance claim is 180 days from the date of the written denial. Missing an administrative appeal deadline is as fatal to a claim as the passing of a statute of limitations with very few exceptions. Missing it means the claim is over, and the denial cannot be challenged.

If the insurance company again denies benefits following a timely administrative appeal (a very common outcome), the claimant can only then file a lawsuit, which must be filed in federal court. State court is without jurisdiction.

THE FEDERAL COURT LAWSUIT…

While beyond the scope of this guide, which focuses on the critical administrative appeal of a claim denial, a bit about the lawsuit that follows helps highlight the importance of the administrative appeal. An ERISA insurance claim lawsuit in federal court is different from others. It doesn’t follow the typical federal procedural path. Most federal district courts use special scheduling orders tailored specifically to the unique way ERISA cases reach court resolution.

ERISA has its own statutory venue rules. Discovery is restricted, really almost nonexistent. The parties have no right to a jury trial. No witness testimony is presented. The only “trial” at all is a trial on briefs referencing the administrative record filed with the court, either on cross-motions for summary judgment or simply motions for judgment on the administrative record.

The court reviews a denial under an “abuse of discretion” standard, requiring it to give great deference to the financially- conflicted insurance company’s decision. Courts have even upheld the insurance company’s administrative appeal decision while expressly stating that it is contrary to how the court would have ruled independently on the evidence.

Choice of venue and choice of law considerations are critical because they can impact the standard of review, as some states have laws prohibiting “abuse of discretion” review, and such laws apply in ERISA cases. Most of the governing substantive law, however, is either ERISA-specific or federal common law jurisprudence, with much disagreement on many issues among and even within federal court jurisdictions.

WARNING 2: But most important, and most pertinent to the impact of the administrative appeal, the federal judge in an ERISA case cannot consider any evidence that was not made part of the administrative record, during the administrative appeal process, before suit is filed.

The insurance companies and their attorneys know this. So they load the administrative record with evidence and reports of their own consulting “experts” favorable to their position in denying the claim.

Most claimants and many attorneys don’t know this. So most claimants and many attorneys file “administrative appeals”, but submit no supporting evidence beyond medical records. They basically argue how unfair the denial is after they paid policy premiums for years. The arguments may be true, but they are not “evidence” that the insurance company or the court must consider. Filing an administrative appeal this way does absolutely nothing to help the claim, and it’s exactly what the insurance company hopes a claimant will do. It wastes the claimant’s best and only opportunity to build the best case for reversal, either on administrative appeal, or in court if the insurer denies the claim again.

But you won’t make that mistake. Instead, you’re going to BUILD a great appeal systematically as follows.

A Step-by-Step Process for a Physician to Win an ERISA Disability Claim – Shredding the Insurance Company Playbook and Beating Them at Their Own Game

The best way for a physician to win an ERISA disability claim or appeal is to build the administrative record evidence far beyond the relevant medical records and argument, and beginning without delay. Without following a set process for doing so, it’s easy to forget to include something important or to lose direction along the way.

So where to start?

The process we follow when representing our physician clients (we call it our Win My Benefits Process), described below, will help guide you to develop and build the nuts and bolts of a strong, well-supported administrative appeal.

1. Calendar your appeal deadline

The law is unforgiving on this. Miss your appeal deadline and your claim is over.

2. Analyze the insurance company’s denial letters

We analyze the reasons given by the insurance company for denying the physician’s claim. This serves as our primary roadmap for what and where our focus needs to be.

3. Analyze the insurance company’s claim file or administrative record

The insurance company is required to provide upon written request, and free of charge, its entire claim file, also commonly called its administrative record. It’s commonly over a thousand pages long. You need to review every page. We always find information there helpful to the case. The file consists of all medical and other evidence the insurer gathered through authorizations you signed, through private investigation, including surveillance video, and the insurance company’s own record review consulting physicians, vocational rehabilitation and other expert opinions and reports. The insurance company is required to include all evidence generated in connection with the claim whether or not the insurance company relied upon it to support the denial.

Much more is there than what is mentioned in your insurance company’s denial letters. We often find evidence that directly contradicts the insurance company’s denial, or a lack of evidence to support a reasons it gave to support a denial.

We have even found evidence that the insurance company’s own expert directly contradicted a denial of our physician client’s benefits. In fact, the court found in one client’s case that the insurance company illegally withheld from my client its own expert’s report, which directly contradicted the denial of benefits. Without reviewing every page of that 1000 plus page record to find the buried report, we would not have found the report, and our client would not have received the benefits she needed and deserved.

(You can Google White v. Life Insurance Company of North America (CIGNA), 892 F.3d 762 (5th Cir. 2018), as revised (Jun 14, 2018) to read the full court opinion. If interested, you can also listen to CIGNA counsel’s and my oral arguments, and the court’s vocal suspicions at winmybenefits.com. You might find it an eye-opener on how far an insurance company will go to avoid a big payout.)

You also need to determine what supportive medical or other available evidence you deem important is not in the record, and include any such evidence as part of your appeal. That way it becomes part of the administrative record which can later be considered by the court if the claim is denied on administrative appeal.

4. Analyze the long-term disability insurance policy, plan and summary plan description

You can request these critical documents directly from the insurance company or the Plan Administrator.

Look at the policy definition of disability. The definition can vary from policy to policy. (See discussion of the different types of “Disability” definitions above.) This definition drives what the physician must prove to be considered disabled under the policy. Most policies have definitions of “Disability” similar to one of the four variations outlined above.

You should also compare the provisions of all other ERISA Plan Documents and Summary Plan Description with those of the insurance policy. Critical definitions or other provisions may differ among the documents to your benefit. We regularly find provisions that directly contradict each other, or provisions that contradict the insurance company’s stated reasons for denying a physician’s claim.

Pay careful attention to the effective dates of the Plan Documents and policy. We sometimes find that the insurance company wrongfully denies a claim based on policy language of an older or newer version of the policy that doesn’t even apply to your case. Or, we may find that the insurance company is seeking to use an unfavorable policy amendment that doesn’t apply to the case at hand to wrongfully deny the claim, or that there is a favorable and policy amendment in effect that the insurance company “overlooked” to deny a claim.

In some cases we find that a provision the insurance company is using to deny a claim is ambiguous, or contradicted by other provisions, making the denial legally unenforceable.

The entire insurance policy and all Plan Documents policy should be read carefully to determine every provision that may undermine the insurance company’s claim denial in any of these ways.

5. List the foundational information supportive of your claim

We like to prepare a formal sworn client affidavit for clients to sign for submission with our disability claims. The content of the finalized statement or affidavit will come from the following.

List all details about your educational background, former work history, physician specialty, and specific physical and mental occupational duties when you became disabled and the nature of the disability. List all physical and mental requirements to perform your specialty, including those required for occasional emergency situations that may arise.

Now list in as much detail as possible exactly what physical and mental limitations you have that hinder your ability to carry out the specified duties of your physician specialty. Describe in detail the nature, intensity, frequency and duration of all pain, physical restrictions and limitations, all mental or physical effects of any prescribed medication, how all of these things affect fatigue, physical functioning, concentration, memory, the need for breaks, rest, sitting or lying down, etc. The more detail the better.

Get your official written job description from your employer’s human resources department and include in your statement or affidavit comments on whether the job in actual practice is different, and if so, how. If the insurance company claim file contains surveillance, it’s imperative that you comment on that as well and include it in your statement or affidavit.

Organize the information in the preceding three paragraphs into the signed affidavit or statement to submit with your appeal.

Next, explore what family members, coworkers or friends can provide affidavits describing their observations of your mental or physical manifestations of disability. Have them prepare appropriate affidavits or statements to sign. They should note their date of birth and relationship to you, and why they have had enough contact with you to accurately comment on your disability. They can say that they’ve read your statement or affidavit and note that it’s consistent with their observations of you, and add any helpful details or examples that come to mind.

6. Gather and analyze medical records to see how well they support the claim for disability and supplement where needed

Gather, review, study and summarize chronologically the relevant medical records, physician reports, diagnostic studies, etc. Here, look for areas of potential strengths, weaknesses or the absence of evidence needed for claim support. The focus is to determine where you need to build evidence that supports disability as defined in the policy, and to address the reasons the insurance company gives to support its denial of benefits.

When your physicians write their reports, they are not necessarily attempting to cover all information in the kind of detail needed to support a disability claim. They often rely on computer programs when preparing their notes that simply do not have fields concerning the evidence necessary to support a claim. So the support needed may be weak or absent from medical records as normally kept. They often don’t state any opinions specifying physical restrictions in enough detail. The insurance companies then cite “lack of evidence” to support the disability. That evidence may in reality exist, but is just not stated well enough in the records. Insurance companies know this and exploit it. Sometimes the records contain plain errors that hurt the claim. These need correcting.

Wherever you find weaknesses, the absence of important evidence or errors in the medical records, correct the problems using a number of different approaches depending on the case at hand.

For instance, you may need to get detailed input from your treating physicians, as well as other medical experts as needed for the particular case. You may need to ask treating physicians to address certain issues not previously addressed specifically and in detail in a report. You may need to push to have certain medical diagnostic tests run to offer unequivocal proof of the existence of a disabling condition. You may need a physician to address in writing the disabling side effects of prescribed medications not previously addressed. In some cases you may need to retain additional physicians of various specialties to provide an opinion.

We sometime meet face-to-face with treating physicians to determine their opinions on relevant details. We sometimes ask them to write a report addressing whether the physician- claimant’s affidavit (to be attached to the report) is consistent with what the treating physician would expect given the medical condition at hand, or whether any surveillance affects his or her opinion regarding disability. Whatever the weakness or absence of evidence or error in the medical records might be, we do everything we can to correct it.

7. Decide what additional evidence may be helpful

At this point, determine what, if any additional medical or other forms of evidence not forming part of the administrative record might be helpful to support the case. This varies from case to case, but may include a functional capacity evaluation (“FCE”) as evidence of the your physical restrictions, further medical diagnostic studies to provide objective evidence of your disabling medical condition, helpful medical records that were simply missing from the insurance company’s claim file, additional affidavits from you, family members or coworkers regarding any important issues that weren’t addressed in initial affidavits, but came to mind afterward.

An expert vocational rehabilitation evaluation is sometimes warranted to rebut an insurance company’s similar expert’s opinion regarding your ability to perform a certain occupation, or what Dictionary of Occupational Titles occupation best resembles your actual job or specialty, or what items the insurance company’s expert failed to consider.

8. Conduct legal research

We conduct nationwide computer research, combing for judicial opinions factually similar or otherwise supportive of the claim and our arguments. Save these so you can later cite to them and quote portions of them to support your arguments to the insurance company, and later to the court if necessary. You might want to retain an experienced ERISA attorney for at least this portion of your claim-building process.

9. Construct the best argument

Again analyze and dismantle the reasons of given by the insurance company for denying the claim. Do this by using everything helpful you find from all of the above efforts, and assemble it into a concise, impactful argument. It should be a blended argument of your strongest facts, woven together with your strongest legal arguments, citing relevant policy provisions, the administrative record and your new evidence which will now be submitted and become part of that record. It should be constructed much like a legal brief filed in court, tailored to follow the same pattern the court will use analyze the case. The insurance companies know by this that you are fully prepared to file suit in federal court in the event of a denial of your claim on appeal.

10. Final review

Before you submit your administrative appeal argument and supporting evidence to the insurance company (which will ultimately be our argument to the court if they deny the appeal), examine your argument again in detail to determine whether it triggers ideas for any additional evidence which may be supportive.

11. Submit the best argument and await a decision

After you feel that you’ve left no stone unturned, and have crafted your very best arguments in favor of the claim, submit your administrative appeal, along with all supporting documentation that was not already part of the original administrative record, to the insurance company.

The insurance company has 45 days to render a decision, with one 45 day extension which it commonly takes (they must give you proper notice to take the extension) to give you a written decision with reasons.

If the insurance company reverses its denial, great! Make sure they calculate benefits and any offsets accurately and for the full period of back pay owed.

If it doesn’t, your efforts and argument will still be useful in the lawsuit that follows. Be sure to request an updated copy of the administrative record and make sure it includes all of the evidence you submitted. This will help to avoid a later argument in court about the completeness of the administrative record to be considered by the judge.

We Hope You’ve Found This Information Helpful…

If you’ve read this page to conclusion, congratulations! You now understand more than most attorneys do about the process of properly handling a physician’s ERISA disability insurance claim.

If you’d like to talk about the particulars of your anticipated or ongoing claim, I’d welcome the opportunity to get on a call or meet with you in person.

To a just and a successful claim result…

Call or text (225) 201-8311 or complete a Free Case Evaluation form